Biography

Ana Zucato is the CEO and founder of Noh, a Brazilian startup building a joint account app for couples. “Noh” means “knot” in Portuguese.

Via Noh, couples can discuss and organize their finances, with the exact same level of permission on both sides. They also receive a card linked to the account.

In 2022, Noh raised a $3M seed round. Ana has over a decade of experience in various tech companies, including roles at Intuit and Truora. To date, Noh has been downloaded around 400,000 times and processed over $60M.

Noh started as a bill-sharing app. What led to the pivot?

Our initial thesis was that Brazil lacked multiplayer financial capabilities. We share everything (Netflix, housing, meals) but payments always rely on a single card. We weren’t certain for which user persona that pain was most acute for however. We gave ourselves a year to test a variety of features, growth hacks… We became known as Brazil’s bill-sharing app.

We then took a few months to analyze the results of these experiments and dive deeper into user discovery. One persona came out on top: couples.

Brazil’s banking infrastructure was built in the 1950s, at a time when women weren’t allowed to own bank accounts. In recent years, Brazil’s outdated bank incumbents have been disrupted by neobanks, Nubank chief among them. But the joint couples account vertical remained underserved.

In traditional Brazilian banks, most joint accounts have an “owner” and a “beneficiary”. The beneficiary, as its name suggests, has restricted access to the account’s functionalities. For certain actions, the beneficiary has to ask the owner for permission. In the case of heterosexual couples, women often held the “beneficiary” title. Many found this setup egregiously unadapted to our times.

That’s for the infrastructure part. The user experience part of joint accounts was also horrendous: my husband and I used to track our joint expenses on Excel, trying to parse them together fairly at the end of the month…

The need for a modern, egalitarian joint account app for Brazilian couples stuck out like a sore thumb. We decided to pivot and focus on that vertical, much to the disappointment of users that weren’t couples.

How is Noh different from other Brazilian neobanks?

For many neobanks, the North Star metric is becoming their users’ primary account. The one where they receive their salary. We didn’t want to play that game because we believed that market to be saturated.

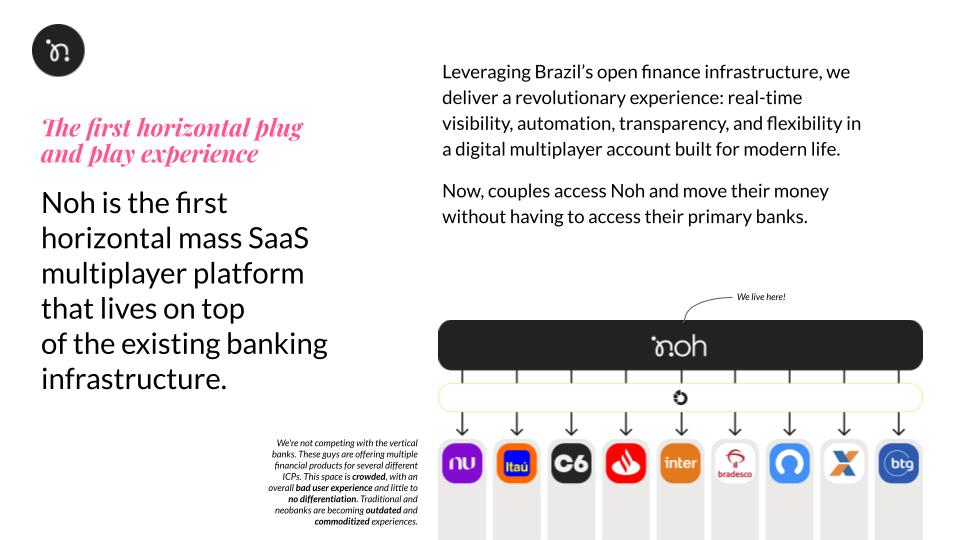

Instead, we built upon recent open banking legislation. Open banking mandates Brazilian banks to open up their data to third parties, enabling said third parties to build better services. Under that same legislation, third parties can also plug directly into banks, making money transfers between banks and third parties seamless for users.

Noh integrates with all major Brazilian banks. Users can easily move their money from their “traditional” account to their Noh account. In the process, we’ve become sort of an overarching account overseeing others. We view Brazilian banks more as commodities than as competitors. Unexpectedly, 40% of our users actually use Noh as their primary account.

Couples on Noh individually top up the account, but the Noh account is truly egalitarian: transparent, with its own card, with the exact same levels of permissions for both users.

Does Noh need any banking licenses then?

We work with a “banking-as-a-service” provider (Dock), which takes on the burden of regulation. This is a revolution in Brazil. Now, fintechs can register as normal corporations and find a banking partner instead of going through the regulatory process themselves. This has saved us millions of dollars and countless months. The money stored on Noh is actually stored with our banking partner.

What are the three, most important Noh functionalities?

The first is that connection with users’ existing banks. Noh is simply a software layer which interacts with one’s bank. The recency of open banking legislation makes this feature novel in the fintech landscape. We’ve been one of the first to ship it.

The second encapsulates the transparency features: each user has equal access, a user can edit the name of a transaction (to clarify what that transaction was for)... Our goal is for users to talk openly about money, the key to healthy communication.

The third is the "envelopes" feature. Couples can create envelopes for specific projects (ie: a trip, buying a house…). They can name those envelopes based on inside jokes they have, allocate money to those projects over time, see them come to reality…

There is no free Noh version. All users pay a monthly fee. Why?

I’ve worked in startups for almost 15 years. I’ve seen startups go under because of the pernicious “we’ll figure out monetization later” trope. It’s unlikely that a user you acquire for free will end up paying.

This can lead to teams burning out, as they desperately attempt to squeeze money out of users who don’t want to pay. Or, the company dies when they can’t raise more money. Or both.

We’ve positioned Noh as a Netflix of sorts, a lifestyle product. We want prospective users to understand that nothing is free. The people building the products they are using need to be paid.

I’d like to exit the era of people thinking software products are meant to be free.

RO insights: subscription model for fintechs

For young fintechs, a subscription model can help prove financial traction quicker than a commission model, especially when initial transaction volume is low.

Here’s how Hassan Bourgi, founder of Ivory Coast’s Djamo, described it to the RO:

“

We operate in francophone West Africa. It’s always more challenging for startups in our region to raise capital. We figured that showing financial traction, not just user traction, early on would increase our fundraising prospects. Due to low initial transaction volume, a subscription model made sense.

Today, we offer a freemium model. Users can use Djamo for free but pay if they want advanced features, such as free money transfers to any wallet or priority customer service. The option to bank for free is a revolution: virtually all regional banks charge their customers a “maintenance fee” regardless of their banking usage.

On top of recurring revenue, a subscription product can boost a product’s usage. If you pay an Amazon Prime subscription, you are incentivized to “use it” and buy stuff on Amazon. It’s the same with Djamo: if you have a premium account, you’re nudged to use our products more.

That increased use benefits us. Merchants pay us “interchange fees” whenever a client uses the Djamo card. In other words: merchants pay us to process payments coming from our cards.

In essence, we run a subscription model but we mostly make money off transaction flows. It’s just that we tap the merchant side rather than the user side.

“

Excerpt from Djamo: banking francophone Africa by the Realistic Optimist

That being said, you’ve explored other revenue streams, such as Noh Multiplica. Tell us more about that product.

Once we had given couples a joint bank account, we explored what other financial needs they might have. Joint investments is one of them.

Arguably, this problem is even worse than the joint account problem. If a couple pools all of their investments into a single account, what happens if the account owner runs away with the money? Or dies? The other person could have their entire retirement money stripped away or be locked in endless judicial battles to recuperate their slice.

We thought about how we could offer joint investment products. Keeping with our ethos, we wanted to own the software, user experience and community layer but not the actual financial services. We ventured out to find a partner.

We found Warren, a fellow Brazilian startup, which helps Brazilians invest. We were aligned on the transparency part. Warren takes a fixed fee rather than a commission, the latter encouraging brokers to push products where their remuneration is attractive but which aren’t necessarily in the client’s interest.

Through Noh Multiplica, couples can invest together via Warren. Warren and Noh then share revenue on new business generated.

Could you extend credit to couples, as a unit?

It’s an interesting challenge. Once again, we’d want to outsource the actual dispensing of the loan, so we’d specialize in credit scoring the couples. We could then sell those credit scores to credit providers.

This opens a new R&D topic. We harbor unique data since we’re pioneering the joint-account neobank play, but joint credit poses questions.

Is the credit line simply the sum of both, individual credit lines? What happens if the couple breaks up? Are they 50-50 responsible for the debt burden? How can you algorithmically predict the chances of a couple staying together, to integrate that risk factor into the credit score?

These are tough questions but if solved, we have a goldmine. Banks and fintechs would certainly be interested in credit underwriting for couples.

What happens if a Noh couple breaks up? How do you return the money?

Couples breaking up is our biggest reason for churn (our current churn stands at less than 5% MoM).

We keep records and track how much money was topped up by who. In the event of the couple breaking up and closing the account, we can divide the money between both users proportionally.

You collaborated with a famous Brazilian financial influencer, Nath Financas. How did that come along and what does the partnership entail?

Nath emailed me on a random Friday evening. She told me she often quarreled with her fiancée about money and saw her own parents divorce because of money. She was passionate about Noh’s mission and wanted to push it forward.

Nath’s audience was exactly the persona Noh is built for: couples turning 30, that don’t have kids but have a pet, have decent salaries but aren’t “rich yet”.

We met up and settled on a media-for-equity deal, where Nath took the lead on our content strategy and production in exchange for shares. She also helps us with product development. The “envelopes” feature was her idea originally and its adoption exploded due to her endorsement and promotion of it.

You said there isn’t much opportunity in the Brazilian fintech infrastructure space, and that opportunities lie in the UX part. Why?

If you look at what the Brazilian Central Bank (BC) has built with both open banking and Pix (Brazil’s real-time payment network), I struggle to see where fintech startups can continue innovating on the infrastructure side.

The popularity of Pix, which is free and instant, has already dealt a blow to card networks (ie: Visa and Mastercard) who specialize in being the intermediary between customers, merchants and each other’s banks. Pix ostensibly replaces them by being quicker and cheaper. Through Pix Garantido, Pix users might even be able to pay for goods in installments, an attractive alternative to credit cards.

Fintech founders in Brazil should focus on exploiting that infrastructure to offer great user experiences rather than compete with the BC on building better rails. Even Nubank’s CEO said he’d be ready to cannibalize their credit card business to build more relevant products on top of Pix.

Brazil’s two recent presidents (Bolsonaro & Lula) are polar opposites. Can’t political turbulence derail Pix’s application?

The BC is independent from the Brazilian government, as is the case for central banks in other countries. As a result, it’s mostly shielded from political skirmishes. It has its own agenda, product roadmap and executes on it. The development of Pix as well as other BC innovations seem quite safe from derailment.

What’s been your worst strategic mistake?

Hiring too many people while we were still looking for product-market-fit (PMF). We shouldn’t have hired a marketing team until we clearly settled on an ICP, for example.

This created tension early on. The company was fast-changing and intense when the team was still frantically searching for our positioning. This wasn’t a good environment for junior team members, since senior team members didn’t have time to spend on proper management. We were all deep in the weeds.

Today, we have a team of just 10, essential people.

What’s your biggest challenge today?

We want to grow 10x and I’m curious about how our current growth tactics will enable us to scale that far. Branding, content and community are great to start. But can they 10x? Can those growth tactics truly scale? There are only so many Instagram influencers you can partner with.

We have to reinvent our marketing and content flywheels to support our ambition.

How important is the feminist aspect of Noh?

I’ve seen data that shows that 7/10 of women are the CFOs of their relationship (in heterosexual couples). If Noh can alleviate the mental load they have from handling that, I’m fulfilled.

One of the questions VCs ask us is whether there’s a feature for one user to block money. What happens if one user uses the couple’s Noh account to gamble? We haven’t had that request from users yet, which is a good sign of the “quality” of couples Noh is onboarding.

It does pose an interesting conundrum however, as such a feature would clash with the “50-50 egalitarian access” ethos that our product encapsulates.

RO insights: startup ecosystems' gender inequality

On top of its product, Noh’s feminist lens is also pushed by its founder being a woman. Still way too rare of an occurrence, in the vast majority of startup ecosystems.

This creates a pernicious cycle which needs to be shortcutted. Here’s how BusCaro’s Maha Shahzad explained it to the RO:

“

I started working in the Pakistani startup ecosystem about a decade ago. My first boss told me that I should do content, because women are “good at writing”. Operational roles were evidently off the table, as they were “men roles”.

This has changed. One of Pakistan’s leading VCs (i2i ventures) is woman-led. I was often the first woman in management positions in the companies I worked at, but that is becoming an increasing occurrence.

We need to shortcut the system. Since the early days of the ecosystem was men-led, the most experienced profiles in the ecosystem today tend to be men, who thus have a better shot at higher roles. The ecosystem needs to collectively spend more time on training and mentoring women.

For women to enter the Pakistani workforce, we need to fix commuting. Pakistani public transport’s rough and dangerous conditions means parents feel safer sending a boy than a girl to school. Professional women might spend an inordinate amount of their salary on commuting, just to access safer and more reliable transportation.

“

Excerpt from BusCaro: reinventing commuting in Pakistan by the Realistic Optimist

What is the Brazilian ecosystem’s biggest flaw? Its biggest strength?

Both are the same. Brazil is a massive country afflicted by a million problems (violence, poverty, corruption). As the saying goes, “good seas never make good sailors”. Many Brazilian founders are operating in a tough environment, tackling tough problems, which makes them of excellent quality.

The Realistic Optimist’s work is provided for informational purposes only and should not be construed as legal, business, investment, or tax advice.