Niko: scaling solar panels in Mexico

Shifting geopolitical currents play in solar's favor in Mexico.

The Realistic Optimist is a B2B paid publication covering the globalized startup scene. It publishes in-depth, written interviews with founders & VCs around the world.

Paid subscribers include teams at Norrsken22, Sturgeon Capital, 54Collective , Goodwell and 500 Global.

Biography:

Raffaele Sertorio is the co-founder of Niko, a Mexican startup helping homeowners and businesses install and finance solar panels. Niko has raised over $26M to date, of which $11M in equity and $15M in debt.

Prior to Niko, Raffaele co-founded Cocinas Ocultas, a dark kitchen company he sold to Travis Kalanick’s CloudKitchens.

What problem are you solving?

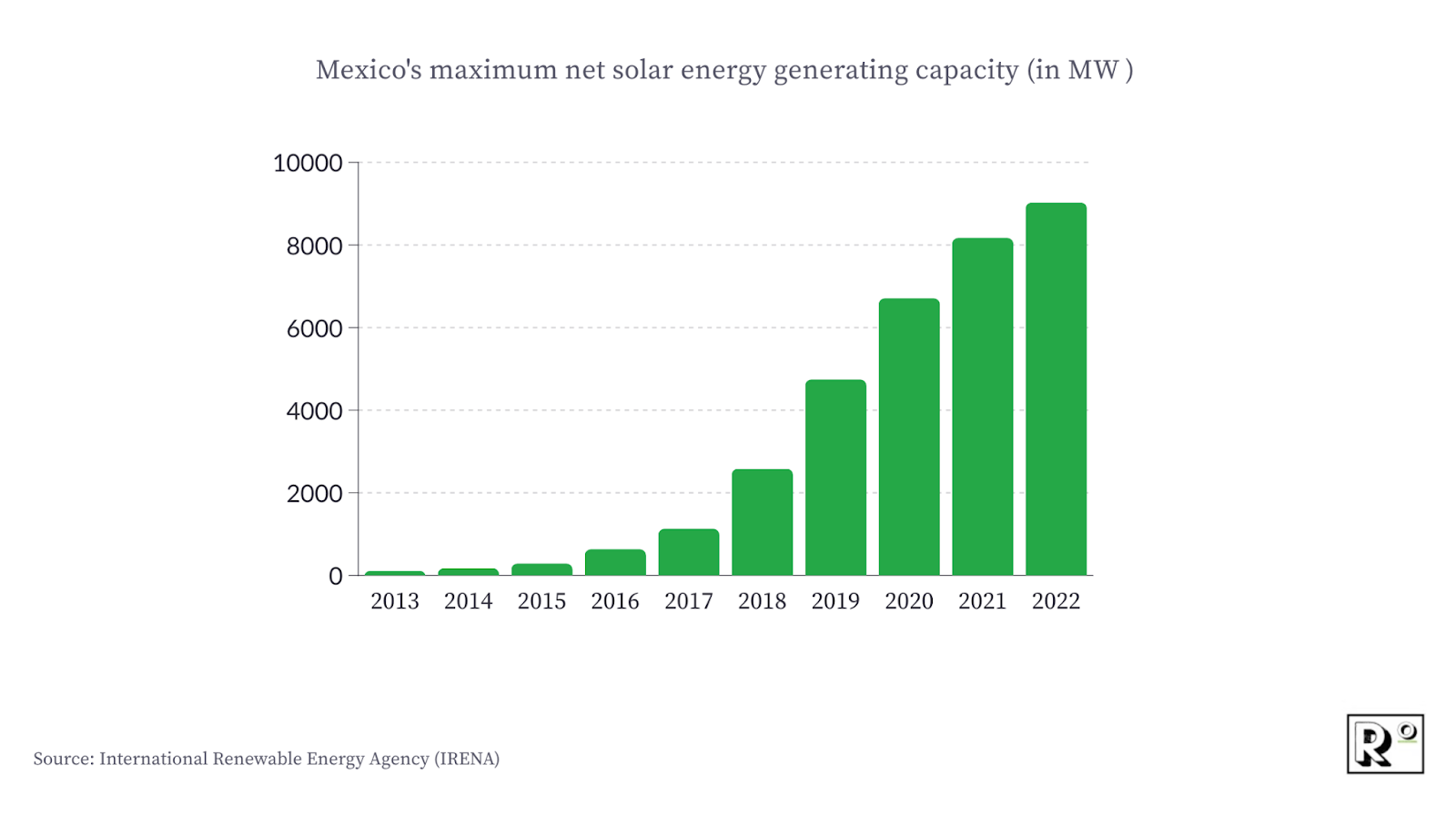

Mexico has increasing energy needs but lags in solar energy adoption. Your average Mexican household doesn’t have enough reliable companies helping them switch their house to solar. The previous Mexican president ran a fossil-fuel friendly administration. This slowed down solar and the governmental incentives needed to boost its adoption.

We’re inspired by what Enpal is building in Germany. We wanted to replicate the model in Mexico knowing that solar here is picking up pace (despite the initial lag). Mexico is one of LATAM’s fastest growing countries in terms of solar energy market size.

We raised from the same VC that funded Enpal’s seed round (Picus Capital). They understood the wave we were preparing to surf and decided to bet on it.

Source: IRENA

How did Cocinas Ocultas start and end?

I’m Italian and spent 7 years working at Credit Suisse in Switzerland. I got bored and felt the entrepreneurial bug biting away.

In 2018, my friend Edoardo Dellepiane and I decided to move to Colombia, which was brimming with opportunity following a peace deal between the government and the FARC (a guerilla group).

We started Cocinas Ocultas, pioneering the dark kitchen concept in South America. A couple of years in, we got acquired by CloudKitchens, founded by Uber’s founder Travis Kalanick. We spent some time being Travis’ right hand, launching markets across LATAM, reorganizing operations in Korea and India… We lived nomadically, jumping from market to market depending on where the company needed us.

After riding out our earnout period, my co-founder and I took a sabbatical. Soon enough, the entrepreneurial bug reappeared and we were back to the races, co-founding Niko.

Summarize the Niko product for us.

We help Mexican homeowners and businesses install and finance solar panels for their homes or their offices.

Our pitch is that solar power is cheaper than relying on the “traditional” grid. Niko customers eventually own the solar panels and gain the possibility to “sell back” the energy produced to the grid, further reducing their energy costs.

Let’s start with the B2C (homeowners) vertical. What are the different payment plans?

The first option is to buy the solar panels at once, upfront. The price tag is between $7-10K (USD).

The second option is to pay in twelve installments, without interest, a popular way of paying for high-value items in Mexico.

The third option is “rent-to-own”, where the customer pays back the panel over 7 years but owns the panels at the end of those 7 years. Our pitch is that the monthly payments they make for the panels are less than their current monthly electricity bill. We estimate the panels to have a life span of minimum 25 years.

Today, I would say 50% of customers opt for the third option, 30% for the second option and the rest for the first option.

In option 2 and 3, Niko buys and installs the solar panels before the customer pays in full. How do you finance that?

On top of our equity money, we’ve raised a $10M debt facility from a local greentech investor and additional $5M from another local debt investor. Thankfully, we raised debt in local currency, so the Mexican peso’s fluctuation isn’t a problem.

RO insights: startups raising debt in emerging markets

For a startup earning money in a volatile currency, raising debt can be tricky. If they raise debt in $USD but make money in local currency, a sudden local currency depreciation could be catastrophic. Their revenue would instantly fall in $USD terms, making it harder to reimburse the debt.

Raising debt in local currency seems like a good alternative. Here’s how Mahmoud El Zohairy from Egypt’s Camel Ventures explains it:

“If the companies we finance make money in Egyptian pounds, we’re going to lend in Egyptian pounds. Lending in USD to companies making money in a depreciating Egyptian pound increases their debt burden as well as their default risk. A depreciating pound means that their revenue continuously loses USD value. The vast majority of our LPs are Egyptian banks, so this strategy makes sense for us.”

Excerpt from “On venture debt in Africa”, originally published in The Realistic Optimist

Isn’t there a risk of over-leverage, since the faster you grow the larger your debt gets?

It’s a risk. There are ways to mitigate it.

The first is by solidifying our underwriting requirements, ensuring that we aren’t lending to people who can’t pay back.

Second, we aim to protect the company by setting up Niko’s debt as “non-recourse debt”.

How does that work?

Niko’s debt providers wrap up the debt in special-purpose-vehicles (SPVs), with the collateral being the solar panels a client purchased. In the case of a default, the debt provider only has a claim over the SPV’s underlying asset, not Niko’s assets.

This dissociates the debt from Niko as a company. This financial setup has been used by Enpal as well.

The “CFE” is mentioned multiple times on the website. What does that refer to?

The Comisión Federal de Electricidad (CFE) is Mexico’s state-owned electricity provider. It’s a monopoly, producing the majority of the country’s electricity.

One of the administrative complexities of switching to solar is dealing with the CFE. Generally, houses are connected to CFE’s grid. At the end of the month, CFE calculates how much you contributed to the grid versus how much you consumed. You are charged accordingly.

The difference with solar is that you now have a house that produces electricity and can contribute to the grid, so the equation flips. Your house’s CFE meter needs to become bidirectional to account for that change. In many cases, your house’s meter is out of date and needs to be replaced.

This entire process represents a 3-6 week administrative process (including the potential installation of the new meter), which we take care of for our clients.

You’ve also opened up a B2B segment: why do B2C and B2B at such an early stage?

We started with a B2C focus because that’s the market’s underserved vertical. Large, industrial solar panel projects (ie: solar panels for factories) were already underway and we didn’t want to compete there.

As time went on, we received inbound B2B leads. Not from large companies, but from small stores. The B2C customer buying solar panels for their house might also want to buy solar panels for the shop or restaurant they own. In both cases, reducing their energy bill is a pertinent value-proposition. From a technical standpoint, this doesn’t add any complexity (it still comes down to installing solar panels on a roof). We decided to welcome those customers as well.

We stumbled upon this underserved B2B niche. While the Nissan factory might already be served , the scattered, small Nissan dealerships across the country aren’t. That’s who we’re targeting.

Do you think that you’ll switch to 100% B2B?

No, because the B2C tailwinds are getting stronger.

Mexico is facing a huge increase in energy demand, in large part due to nearshoring. The US wants to decouple its industrial supply-chain from China, but can’t switch the products it consumes from a Chinese cost base to an American cost base. Products would become unaffordable to American consumers.

The best second option is Mexico, which recently passed China as the US’s biggest trading partner. Chinese corporations are opening factories in Mexico, circumventing the US’s new restrictions. This creates a boom in Mexican industrial activity (and thus a boom in electricity demand).

RO insights: when geopolitics opens new trade corridors

Geopolitical developments can reshape trade routes, as countries reduce reliance on specific countries or sanction them outright. Sagacious founders identify those shifting currents and build upon them.

Here’s how Niko Turabelidze, co-founder of Georgia’s Cargon, explains how the war in Ukraine impacted his market:

“It has reinforced the importance of the region we cover.

Now, goods transiting by road from China to Europe or vice-versa have to travel via Central Asia and the Caucasus. Indeed, the southern corridor (Iran) has been sanctioned for years and Ukraine’s invasion means the northern one (Russia) is sanctioned as well.

This has increased investment flows towards the region’s logistics infrastructure. Kazakhstan and the Caspian Sea in particular have gained clout. The US has a federal financing program aimed at the Central Asian corridor.”

Excerpt from Cargon: Flexport for Central Asia, originally published in The Realistic Optimist

How does this translate to B2C tailwinds?

Because the Mexican government wants to free up the grid’s electricity to power that manufacturing growth. The government is incentivized to help homeowners produce their own energy through solar and reduce their reliance on the grid.

With time, I believe we’ll move towards a virtual power plant (VPP) model, where solar panels on homes and offices’ act as nodes in a decentralized grid, intelligently pushing and pulling electricity as needed.

How does Niko make money?

We buy solar panels for less than we sell them, “hardware margins” essentially. One of the reasons we picked this sector is for its healthy margins (margins are higher in the B2C context, due to scarcer competition in that segment). We’re quite happy with the hardware margins we’re making for now.

We also make limited money on our lending product (we charge a spread between the interest on what we borrowed versus what we lend out to customers). This is in addition to our hardware margin - relying on the lending spread only puts the business at risk of rising interest rates. If the cost of my debt goes way up, I have to correspondingly charge higher interest on my customers, which might kill growth.

Our highest margin product is Niko Care, a sort of “Apple Care” for clients’ solar panels. A subscription buys a client preventive and reactive maintenance of their solar panels. Many things could damage a client’s solar panels, such as a golf ball or a bullet.

Where do you buy the solar panels from?

We work with 4-5 reliable Mexican distributors of Chinese solar panels. We don’t have the sales volume to source directly from China yet but when we reach that stage, we should attain even higher margins.

What’s your thorniest operational challenge?

Finding high-quality solar installers to install the panels we sell. This industry is still new in Mexico, so the corresponding talent pool is still thin.

We’ve decided not to rely on the limited number of companies offering such services (they prioritize their bigger clients over us) and have started building our own internal payroll of Niko technicians. We can still outsource “blue-collar” functions (ie: picking up the solar panels, physically installing them) but we need a Niko engineer to oversee the entire process.

What are prospects’ most common reluctance to buy from Niko?

There are two main barriers.

The first is that the Mexican zeitgeist regarding solar panels and solar energy isn’t always in our favor. Some doubt a Chinese product can be sturdy enough. Others read on social media that solar energy is a fraud. There’s a fair amount of customer education to do.

The second is cost. Mexican consumers are extremely price-conscious, sometimes to a fault. Everyone knows a handyman that could, in theory, find and install solar panels for cheaper than Niko. But that handyman doesn’t have the professionalism we bring and installing a solar system is more complex than fixing your washing machine. That handyman won’t do the CFE paperwork and a solar system that isn’t connected to the grid is useless (because you can’t sell back the energy to the grid).

I’ve heard countless horror stories of clients coming back to us after initially choosing the handyman, because the handyman messed up. This is even the case for clients with $10M homes, who still opt for the cheaper option initially regardless of the associated risks, and then call us in to fix it.

Do you have any competition?

All VC-backed solar players are focused on C&I (commercial & industrial), while we compete with the perennial handyman and local construction companies.

There’s such a boulevard of clients to serve that there’s space for other startups to compete alongside us.

What metrics are you most and least proud of?

I’m proud of our growth and our healthy margins. It’s encouraging because we generate a fair amount via word of mouth while being a little over 1 year old.

I’m frustrated by our speed of installation. We aim for it to be 3 weeks from the moment the client signs, but in effect we hover around 6 to 8 weeks, because of the installation talent bottleneck I mentioned earlier.

What’s been your biggest strategic mistake?

We were stubborn about keeping our hardware margins sky high (around 40%). We realized that this hurt our growth and that we could still be profitable with lower margins. The more we grow, the higher our purchasing volume and the heftier discounts we can get (which ultimately turn into higher margins).

What foreign proxy are you modeled after and what have you had to localize?

We were clearly modeled after Germany’s Enpal. Now, our vision is to become the Octopus Energy (a leading UK clean energy company) of Mexico.

On the localization front, we’ve decided to move into B2B faster than they did (Enpal is still around 90% B2C I believe) as we saw a terrific and untouched niche in Mexico. Building an internal team of technicians is something Enpal only had to focus on when they reached scale rather than in the early stages, because the German market had a denser availability of competent installation companies.

What’s the biggest structural risk to Niko?

Operational risk, first and foremost. Many things can make us lose money: we grow too quickly and aren’t ready to fulfill demand on installations, borrowers can’t pay us back…

An economic recession could hurt demand for Niko’s product. Trump supposedly wants to impose crushing tariffs on Mexican products which, if materialized, would be nefarious. I doubt the entirety of his threats will come to fruition because goods coming from Mexico are replacing goods the US used to source from China. The US will only go so far in curbing the import of those Mexican goods, because they’re dependent on them.

Lastly, there’s political risk. The CFE, which is government-owned, is in a monopolistic position. They can do what they want. If they drastically reduce the amount they pay for the solar energy our clients pump back into the grid, that erodes our value proposition. I’m not too worried because Mexico needs more energy, CFE knows that and it isn’t in their interest to curtail the growth of solar and the new government has been saying quite the opposite.

That being said, CFE represents a lot of jobs (so it’s a vote machine) and the effective deployment of solar could theoretically reduce CFE’s headcount. That’s something we’ll have to aptly navigate (although we’re far from the scale for that to be a problem).

Source: SENER via S&P Global

Mexico recently elected a new president, Claudia Sheinbaum. How does that election change the political winds for Niko?

It’s a paradigm shift. Sheinbaum has a PhD in energy engineering. Even though she’s from the same party as her fossil-fuel focused predecessor, her energy policy is entirely different. She’s definitely more pro-solar than AMLO (Mexico’s previous president).

What could really move the needle is privileging subsidies targeting the installation of solar panels rather than subsidies directed to simply reduce one’s utility bills. It’s a more sustainable, effective long-term solution.

What do foreign investors deeply misunderstand about Mexico’s startup scene?

This isn’t something investors misunderstand but a useful observation.

Many founders in LATAM were quite traumatized by how VCs acted when the funding market crashed, post-2021. Founders felt unsupported during very hard times. As a result, they are now very selective about who they let onto their cap table.

A good selling point for a VC wanting to invest in LATAM founders is a proven track record of staying close to its portcos when times got rough.

The Realistic Optimist’s work is provided for informational purposes only and should not be construed as legal, business, investment, or tax advice.

Want to purchase a Realistic Optimist subscription for your team? Email tim@realisticoptimist.io